Capitalization and Reconciliation

Content

- How to Calculate the Beginning Work-in-Process Inventory

- References – Buildings and Improvements

- How to Handle Work in Progress (WIP) or Construction in Progress (CIP) in QuickBooks

- Financial Management: Overview and Role and Responsibilities

- NetAsset Makes CIP Process and Roll Forward Reports Easier in NetSuite

- What is construction in progress (CIP)?

All materials and content were prepared by persons and/or entities other than Lorman Education Services, and said other persons and/or entities are solely responsible for their content. Unbilled Receivable means, at any time, any Receivable as to which the invoice or xxxx with respect thereto has not yet been sent to the Obligor thereof. You can track CIP assets in Oracle Assets, or you can track detailed information about your CIP assets in Oracle Projects. 1) On March 11, 2021, Business A received a $100,000 bill from Builder’s Warehouse for construction materials.

- The difference between WIP and finished goods is based on the inventory’s stage of relative completion, which, in this instance, means saleability.

- However, costs that are incurred to change the long-lived asset from one intended use to another , would generally not be capitalized.

- These types of costs generally do not extend the useful life of the asset or improve the quantity or quality of goods produced by the asset.

- The accounting for costs to arrange financing for the construction of a new capital project is specifically addressed by ASC 835, Interest.

- The term „12 months rolling” refers to a method of tracking and analyzing data over a period of time that moves forward by 12 months at the end of each month.

Normally, upon completion, a CIP item is reclassified, and the reclassified asset is capitalized and depreciated. Is the process accountants use to track the costs related to fixed-asset construction. Because construction projects necessitate a wide range of prices, CIP accounts keep construction assets separate from the rest of a company’s balance sheet until the project is complete. You book 15 invoices for the parts and labor to CIP related to this project. In NetAsset, you can simply filter for this project, select the 15 transactions (vendor bill, journal entries, etc.), then capitalize the asset. The system gives you the option to create 15 separate assets or one single asset.

How to Calculate the Beginning Work-in-Process Inventory

However, there can be thousands or even hundreds of thousands of moving pieces which make the report very time-consuming and prone to error. For businesses with more than 10,000 assets, or those utilizing the power of Microsoft SQL Server, FAS 500 CIP Accounting provides speed, scalability, and control over your construction in progress projects. General and administrative costs and overhead costs should be charged to expense as incurred. Capitalization of ground lease expense by a lessee for property constructed for its own use is prohibited. However, ground lease expense should be capitalized during the construction of property for sale or rental.

Accordingly, given the high degree of uncertainty about the future economic benefits, costs incurred during this stage are expensed as incurred. The costs of constructing the asset are accumulated in the account Construction Work-in-Progress until the asset is completed and placed into service. When the asset is placed into service, the account Construction Work-in-Progress will be credited for its balance and will be recorded with a debit in the appropriate property, plant and equipment account. After the construction has been completed, the relevant building, plant, or equipment account is debited with the same amount as construction in progress.

References – Buildings and Improvements

These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in oureditorial policy. NetAsset also provides depreciation waterfall reports to help with forecasting, reconciliation reports to help with month end, and financial/subledger reports to help with internal and external reporting.

- Another objective of recording construction in progress is scrutiny and audit of accounts.

- The useful life of an asset is considered extended when the change to the asset is significant enough to cause the expected useful life to increase beyond the original estimation.

- You are now ready to place the asset in service and start depreciating.

- A construction company might come to your mind by reading the phrase “Construction In Progress.” Indeed, construction in progress accounting is mostly used by construction firms.

- PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network.

The IAS 11.9 regulates the treatment of two or more assets’ construction as a single contract if they are negotiated as one contract. Projects that have reached substantial completion will be capitalized from CIP to full capital assets by CAM. CAM will lead the effort to componentize building components as appropriate. On a monthly basis, CAM will reconcile the capital asset balances in the PeopleSoft Asset Management system with balances in the General Ledger system. Reconciliations shall be maintained and available for audit purposes. Accounting in the construction industry isunlike most other industries.

How to Handle Work in Progress (WIP) or Construction in Progress (CIP) in QuickBooks

General and administrative costs should be expensed as incurred, with a limited exception related to property constructed for sale or rental. Once the project is probable, directly identifiable costs should be capitalized. The amount capitalized construction in progress accounting is limited to those amounts directly related to the site and project selected (e.g., costs related to evaluation of potential projects or locations should be expensed). Changes to the capitalization threshold should be applied prospectively.

In certain circumstances, there may be depreciation costs directly related to the construction project, such as depreciation of equipment used to build a long-lived asset for internal use. The depreciation costs of the equipment used to build a long-lived asset are considered directly identifiable and should be capitalized. On the other hand, depreciation related to the company’s headquarters would be considered an indirect cost and should be charged to expense as incurred. The first stage during which costs are incurred related to long-lived assets is the preliminary stage. During the preliminary stage, the project is not considered probable of being constructed.

Financial Management: Overview and Role and Responsibilities

It is standard practice to minimize the amount of WIP inventory before reporting is necessary since it is difficult and time-consuming to estimate the percentage of completion for an inventory asset. Figure PPE 1-1 summarizes general accounting guidance for costs that are typical with capital projects. This summary is provided for informational purposes only and should be considered in the context of the applicable guidance and the reporting entity’s specific facts and circumstances. It should also be read in conjunction with the guidance provided throughout PPE 1.2.

What type of asset is CIP?

A construction-in-process (CIP) asset is an asset you construct over a period of time. Create and maintain your CIP assets as you spend money for raw materials and labor to construct them. Since a CIP asset is not yet in use, it does not depreciate and is only in the corporate book.

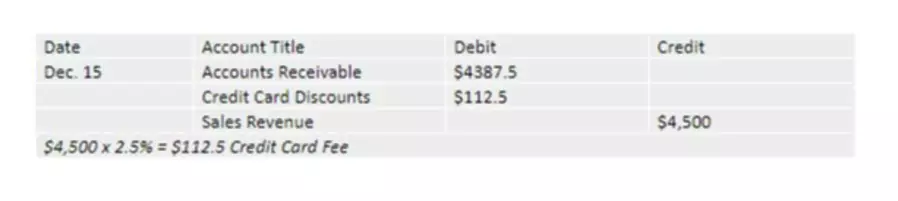

You would take the accounts receivable balance as of December 31, 2021, and add any new sales invoices created in January 2022. You would then subtract any payments received in January 2022 from customers for outstanding invoices as of December 31, 2021. The resulting total would be the accounts receivable balance as of January 31, 2022. What if you could have your accounting software generate this report for you? NetAsset provides an out-of-the-box fixed asset roll forward that is systematically generated so neither you nor your auditors need worry about the accuracy of the report.

Manufacturing Corp is expanding its manufacturing footprint by constructing a facility in China. The facility has been completed and is producing prototype parts, which are being tested to ensure they are in accordance with the customer’s quality specifications. Incremental direct costs of PP&E pre-acquisition activities incurred for the specific PP&E in transactions with independent third parties.

- In the company’s balance sheet, construction in progress is most commonly found under the head of PP & E( Plant, Property & Equipment).

- It is standard practice to minimize the amount of WIP inventory before reporting is necessary since it is difficult and time-consuming to estimate the percentage of completion for an inventory asset.

- Refer to PPE 4.3.1 for additional information on the commencement of depreciation.

- This covers everything from the overhead costs to the raw materials that come together to form the end product at a given stage in the production cycle.

- For example, the cost to run machinery and equipment in order to test that the output meets certain regulatory specifications would be considered costs of the construction stage and should be capitalized.

The difference between WIP and finished goods is based on the inventory’s stage of relative completion, which, in this instance, means saleability. WIP refers to the intermediary stage of inventory in which inventory has started its progress from the beginning asraw materialsand is currently undergoing development or assembly into the final product. Finished goods refer to the final stage of inventory, in which the product has reached a level of completion where the subsequent stage is the sale to a customer.